The UAE has never been shy about its love for cars. From daily commutes across emirates to weekend desert drives, mobility here is not a luxury. It is infrastructure. But in 2026, the UAE car market financing landscape has shifted in subtle ways. The real engine powering car sales may not be horsepower or hybrid innovation. It may be financing.

Over the past few years, vehicle prices have climbed steadily. Advanced driver assistance systems, hybrid powertrains, larger infotainment screens, and safety upgrades have pushed sticker prices upward. At the same time, auto loans, long-term installment plans, low down payments, and promotional interest rates have become standard practice.

For many buyers, the question is no longer, “Can I afford this car?” It is, “Can I manage the monthly EMI?”

That distinction matters more than it seems.

Why 2026 Feels Different

The UAE car market has always thrived on aspiration. But today the conversation has moved from performance figures to payment structures.

Over the past five years, three clear shifts have taken place.

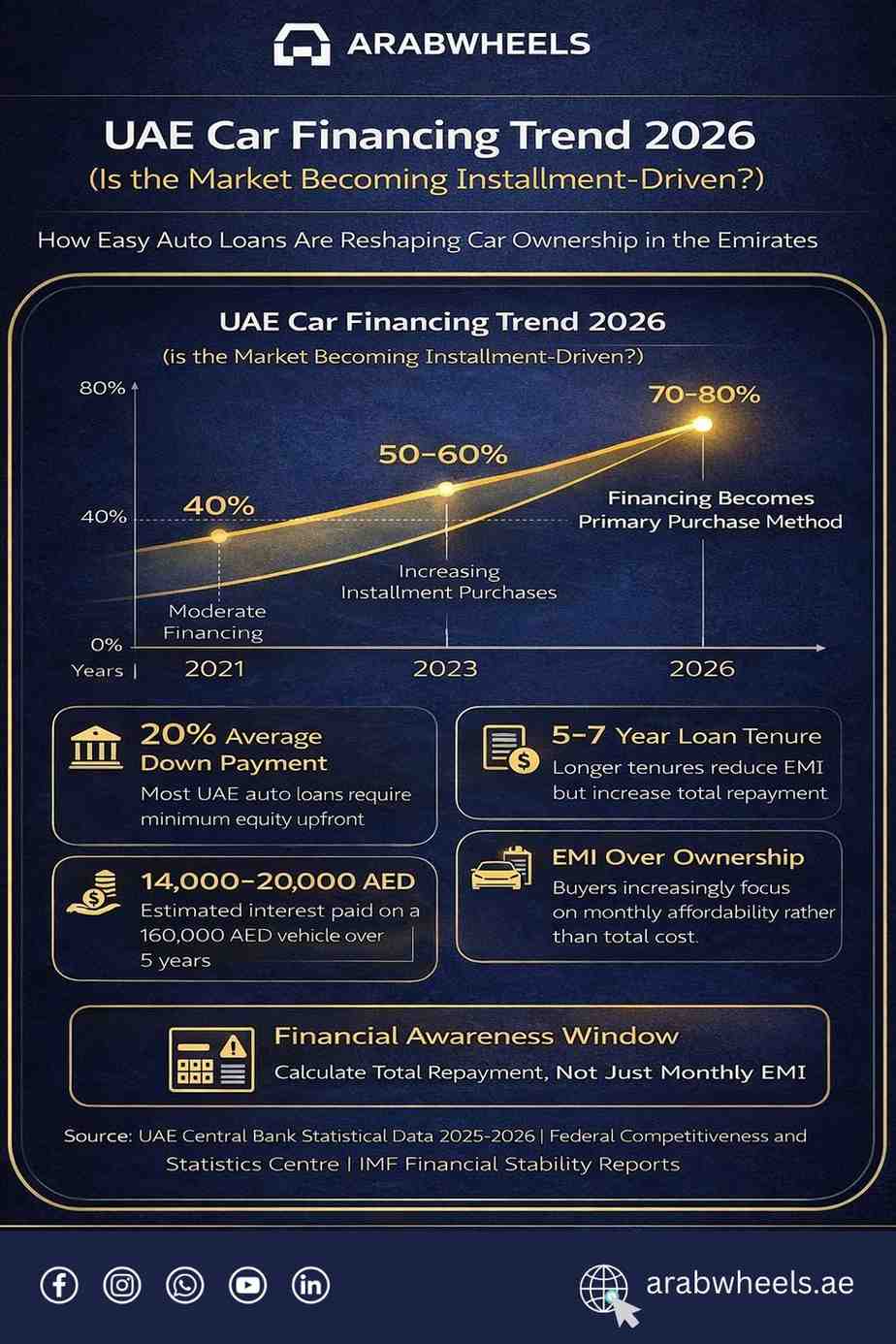

Auto loan portfolios have expanded steadily, reflecting the growing reliance on structured credit. At the same time, average vehicle prices have climbed from roughly 120,000 AED levels to well above 150,000 AED in many segments. Loan tenures, once typically 4 to 5 years, are now stretching to 5 to 7 years.

Global supply chain disruptions, semiconductor shortages, and inflation have contributed to higher vehicle costs. The shift toward hybrid and electric vehicles has added another layer of expense. In response, lenders have aggressively expanded auto financing. Longer tenures, balloon payments, bundled insurance, and flexible repayment options are now common.

According to data published by the UAE Central Bank, auto loans remain one of the largest components of the country’s consumer lending portfolio. Transportation-related costs tracked by the Federal Competitiveness and Statistics Centre also reflect upward pricing pressure across the sector.

The result is clear. More vehicles are being sold, but increasingly through credit rather than outright ownership.

Financing is no longer helping the market. It’s holding it up.

What Buyers Are Really Paying

A typical mid-range vehicle priced between 130,000 and 180,000 AED often requires a 20 percent down payment and a five-year tenure. Interest rates typically range from 2.5 percent to 4.5 percent, depending on the credit profile.

On paper, the monthly installment feels manageable.

But let us examine a simplified example:

- Vehicle price: 160,000 AED

- Down payment: 32,000 AED

- Loan amount: 128,000 AED

- Estimated interest over five years: 14,000 to 20,000 AED

- Total paid: 174,000 to 180,000 AED

That difference may not feel dramatic month to month. Over five years, however, it adds up.

Now multiply that pattern across tens of thousands of vehicles annually. The structure begins to resemble a subscription economy more than traditional ownership.

Why Financing Is Booming

This shift is not irrational. It is structural.

- First, vehicle prices have risen faster than average salary growth. Financing bridges that gap.

- Second, banks favor auto loans because they are secured assets and carry lower risk than unsecured personal loans.

- Third, mobility in the UAE is not optional. Inter-emirate travel, school runs, and long commutes make private transport essential for most households.

- Fourth, hybrid and electric models carry higher upfront costs. Financing smooths entry into these new technologies.

In that sense, financing is a rational response to price pressure. The real question is not why financing exists. It is how dependent the market has become on it.

Healthy Growth or Quiet Risk?

When a market leans heavily on credit, three long-term effects often appear. Price insulation occurs because buyers focus on monthly affordability rather than total cost. That reduces resistance to higher vehicle prices.

Debt normalization sets in. Younger buyers enter multi-year financial commitments earlier and more frequently. Interest rate sensitivity increases. If borrowing costs rise sharply, demand can cool quickly. The UAE banking system is tightly regulated, and non-performing loan ratios remain relatively contained compared to many global markets.

There is no immediate sign of systemic stress. But credit-driven demand is inherently more sensitive to economic cycles than cash-driven demand.

The Used Market Tells a Story

Another signal of dependency is evident in the used-car segment. Pre-owned vehicles were once largely cash transactions. Today, installment options are common even for older models.

This changes buyer psychology. The decision framework shifts from “What can I afford outright?” to “What fits my monthly budget?”

That subtle shift reshapes pricing dynamics across the entire auto ecosystem.

The Five-Year Perspective

Consider a simplified five-year ownership comparison:

| Cost Component | Financed Mid-Range SUV | Cash Sedan Purchase |

|---|---|---|

| Vehicle Price | 160,000 AED | 110,000 AED |

| Interest (5 years) | 15,000 AED | 0 AED |

| Insurance (5 years) | 8,000–10,000 AED | 6,500 AED |

| Maintenance (5 years) | 6,000–9,000 AED | 5,500 AED |

| Estimated Total Outflow | 189,000–194,000 AED | 122,000 AED |

The difference is not just about vehicle size. It is about leverage. Financing increases purchasing power. It also increases long-term exposure.

Are Buyers Overleveraged?

There is no evidence of a credit bubble in UAE auto lending. Regulatory caps on debt burden ratios help prevent excessive borrowing. Banks assess income stability carefully.

However, lifestyle inflation is real. High-end trims, technology packages, and premium upgrades often stretch budgets because financing makes them feel accessible. When the focus remains solely on EMI size, awareness of the total cost of ownership fades.

The issue is not whether financing is good or bad. The issue is whether buyers are evaluating total ownership cost, including interest, depreciation, insurance, inflation, and resale value. That calculation is where real financial intelligence lies.

So, Is the Market Too Dependent?

The UAE car market in 2026 is undeniably financing-driven. But dependence does not automatically equal instability. The system remains regulated. Credit quality remains stable. Consumer demand remains strong.

Yet sales volumes are clearly sensitive to credit conditions. If interest rates shift or lending policies tighten, demand could respond quickly. In simple terms, financing is no longer a convenience. It is the engine. And engines, while powerful, require careful calibration.

Final Take

The UAE car market is not in crisis. It is not in a bubble. But it is operating on a model where access to credit plays a central role in sustaining momentum. Financing can unlock opportunity. It can also mask the true cost of ownership.

In 2026, the smartest buyers will look beyond monthly installments. They will compare total repayment, resale projections, fuel efficiency, maintenance costs, and depreciation curves. Because in the long run, affordability is not about what you pay each month. It is about the total you pay.

Before signing your next car loan, run the full numbers. Compare financing structures, ownership costs, and long-term value. Explore expert insights, car comparisons, and real market analysis on ArabWheels to make decisions that work for your future, not just your monthly EMI.